Influenced by the events of 2022 – including the Russian invasion of Ukraine, high inflation, rapidly rising interest rates, and poor investment returns for both stocks and bonds – the general consensus at the start of 2023 was for another difficult year ahead and the inevitability of a global recession. However, despite central banks continuing to hike interest rates throughout the first half of the year, the failure of multiple U.S. banks, and increasing geopolitical conflicts, capital markets surprised many by performing remarkably well in 2023. As is often the case, “when all the experts and forecasts agree — something else is going to happen.”

Read on for a recap of capital market performance in 2023 and our thoughts on what might lie ahead for investors in 2024.

2023 Performance

Given our passive investment management philosophy, we don’t spend much time analyzing the economic cycle or forecasting short-term returns for individual securities, sectors, or countries. Instead, we focus on long-term return assumptions for broad asset classes and construct model portfolios that we expect will generate efficient returns for our clients in the context of modern portfolio theory.

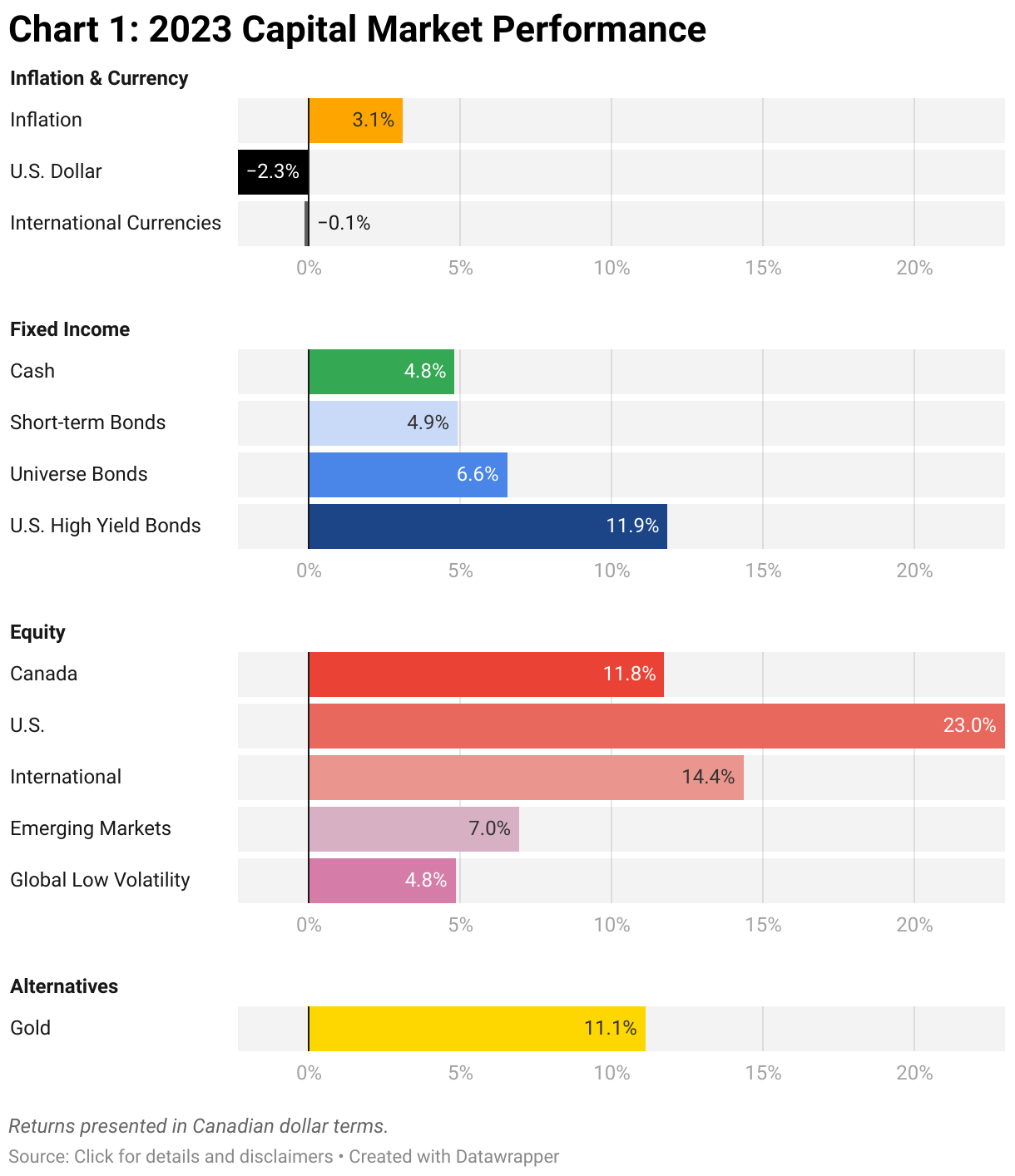

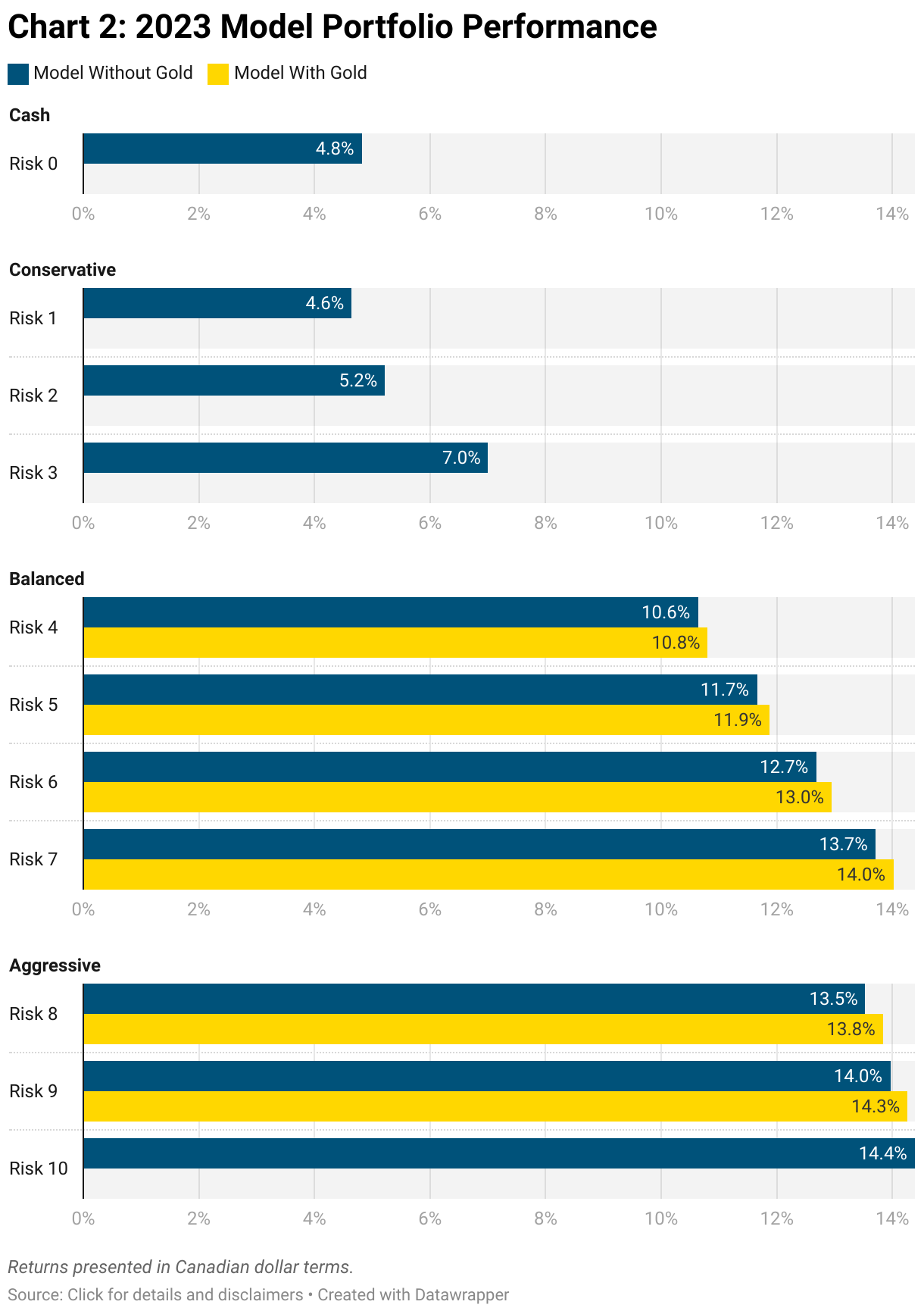

Despite this long-term focus, monitoring the performance of capital markets over shorter time frames can be useful as an assessment of whether investment returns are tracking consistent with our long-term assumptions. Chart 1 outlines the returns for various benchmarks in 2023 while Chart 2 demonstrates how combining those benchmark returns in different proportions – our model portfolios – impacted results last year:

As demonstrated in Chart 1, the past year was quite rewarding for investors, with the majority of asset classes experiencing impressive returns. Unlike 2022 – where stocks and bonds declined in tandem – investors were well-compensated for holding almost any type of financial asset in 2023, be that cash, bonds, stocks, or gold. For more details on why this was the case, click/tap below to expand our commentary on 2023 capital markets performance:

Chart 2 demonstrates that the performance of our model portfolios in 2023 obeyed the typical relationship between portfolio risk level and portfolio return, with higher risk portfolios experiencing better returns for the year than lower risk portfolios. While this relationship does not always hold year-to-year, investors willing to take on more investment risk are expected to be rewarded with higher returns over the long term.

5-Year Performance

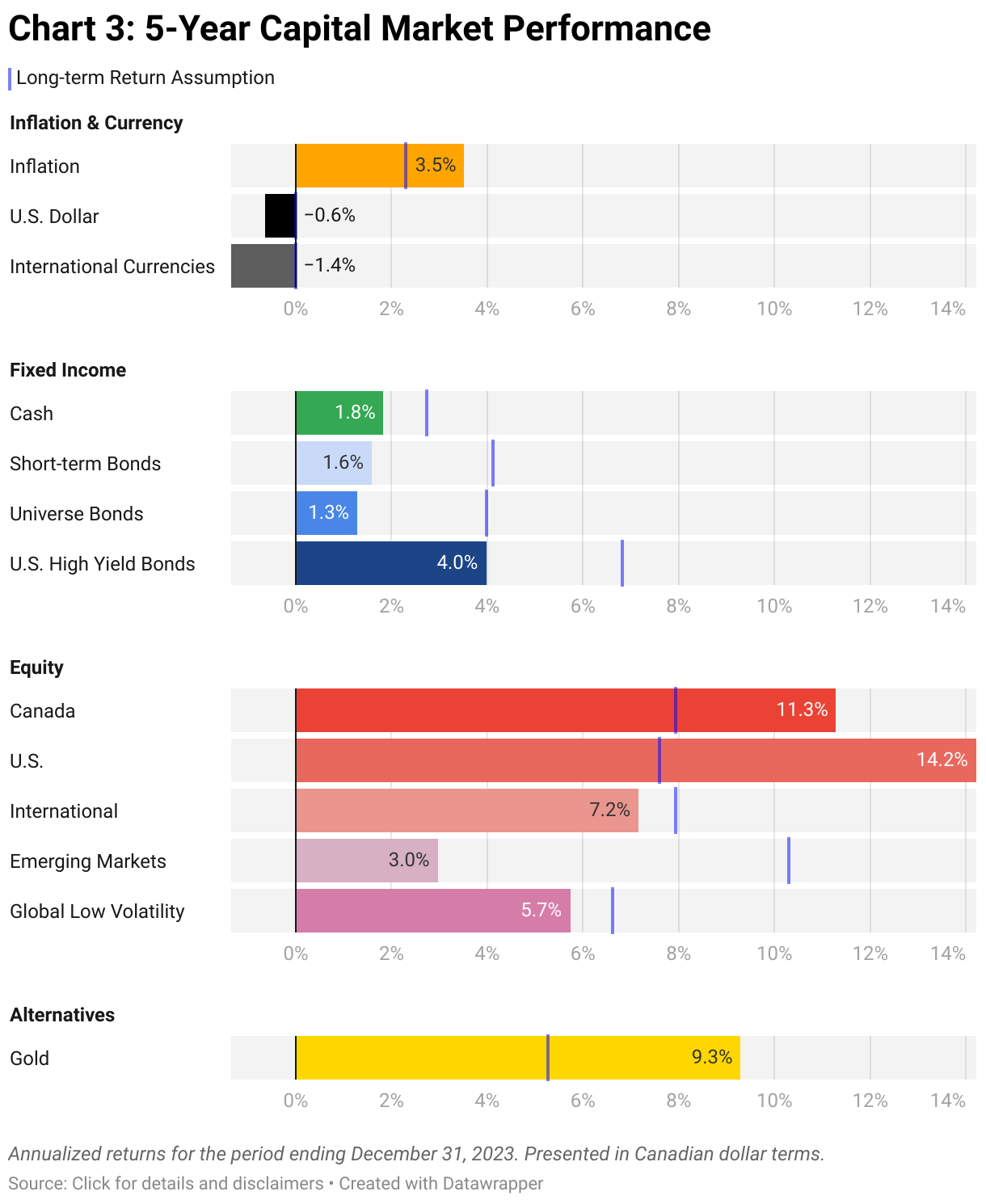

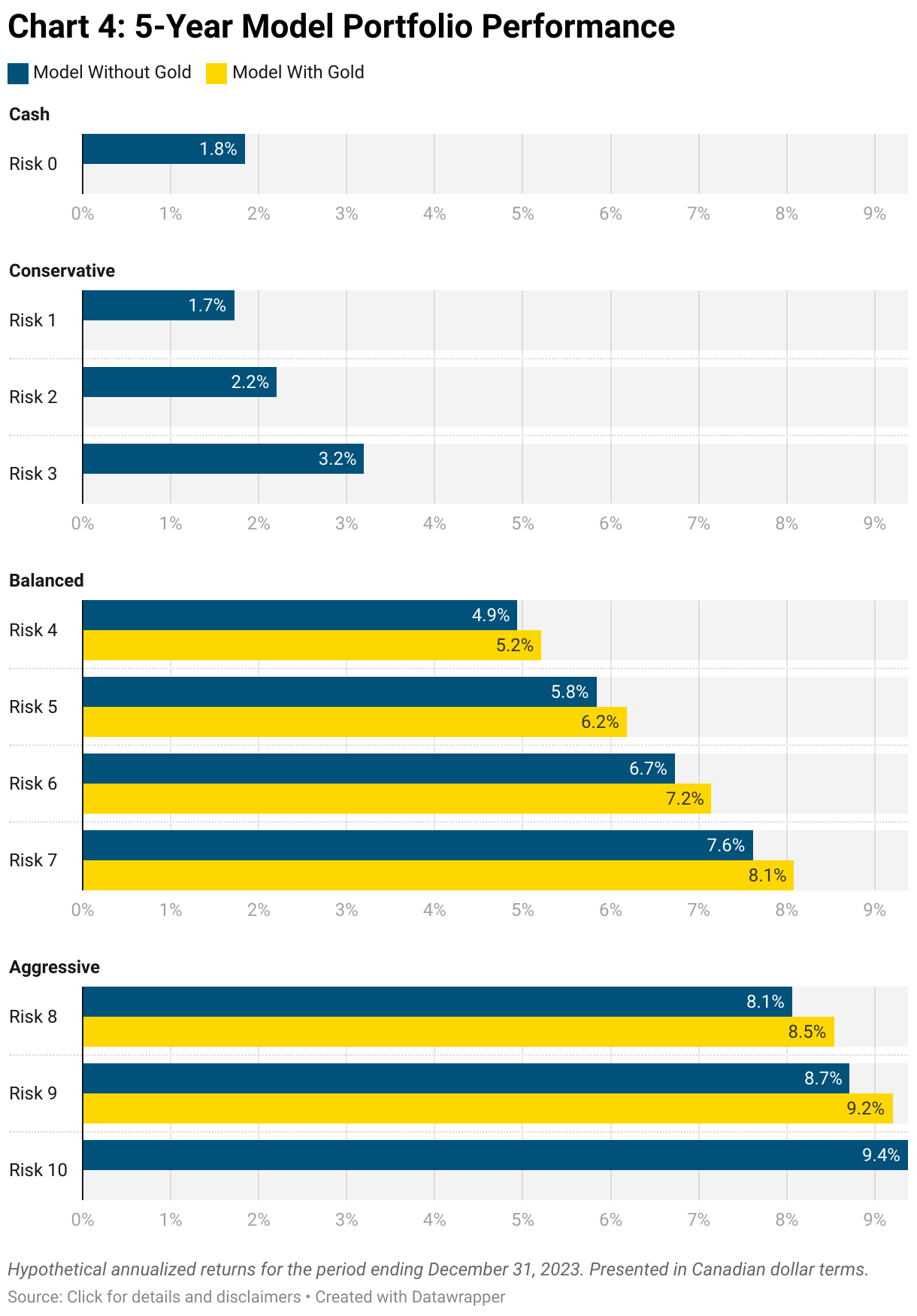

We encourage investors to largely discount the year-to-year swings of capital markets and to instead focus on longer-term results. Charts 3 and 4 therefore present annualized capital market and hypothetical model portfolio performance over the past 5 years:

Given the impressive returns experienced in 2023, the majority of the benchmark returns presented in Chart 3 improved for the 5-year period ending December 31, 2023 compared to the 5-year period ending in 2022. Many of the 5-year benchmark returns are tracking in line (i.e. +/- 2%) with our long-term capital market assumptions (represented by vertical blue lines in Chart 3), but there are some notable exceptions:

Chart 4 demonstrates that the hypothetical 5-year performance of our model portfolios obeyed the typical relationship between portfolio risk level and portfolio return, with higher risk portfolios experiencing better returns over the past five years than lower risk portfolios. Given the impressive returns experienced last year, the 5-year annualized returns for all model portfolios ending December 31, 2023 improved compared to the 5-year period ending in 2022.

Firm Highlights

2023 was a successful year for High Level Wealth Management as we continued to welcome new clients and grew the firm’s assets under management by more than 70% compared to December 2022. We are proud of the fact that most new clients find us through word-of-mouth referrals or by organically searching for alternatives to traditional wealth managers. There is clearly an appetite among Albertans for fair-priced passive investment management services that are delivered in a professional, trustworthy, client-focused manner.

From an operational perspective, our biggest undertaking in 2023 was the transition to a new financial planning software provider. The new tool offers more advanced features and presents information in a more client-friendly manner. Throughout the year, we also continued discussing our new sustainable investment strategies with clients, made small enhancements to the My High Level Wealth client portal, and introduced a new asset class – United States High Yield Bonds – to our model portfolios.

High Level Wealth Management has several priorities in 2024:

- March 2024 marks the 5-year anniversary of our firm’s incorporation. Like most startups, we’ve undergone an incredible amount of change in our first few years, particularly related to the many steps required to receive registration as a Portfolio Manager. Added to this were the unique challenges of operating a business during the COVID-19 pandemic. Thankfully, we’ve now reached a point where our business feels fully established and sustainable. With fewer resources being dedicated to building the basic foundation of our business, we can now dedicate more time and effort to what really matters: improving and expanding our client-facing services.

- A specific focus for 2024 will be enhancements to how we collect client information. Currently information is typically collected via email or during regular review meetings. We will begin work on a “client profile” module in our client portal that will enable clients to provide their personal information – and keep it up to date – in an efficient and well-structured manner.

- Improving the user experience of our client portal on mobile devices remains a priority, as does converting several reports from standalone spreadsheets to interactive client portal modules. Your feedback on our client portal is always appreciated, so let us know if you have any ideas, criticisms, or opinions.

- Introducing our services to new clients also remains a priority. It is hard to assess in advance what our maximum capacity will be for bringing on new clients, but we are always conscious of our limits and continually assess whether we can continue bringing on new clients without adversely affecting the level of service provided to existing clients. At this point we estimate that we are at about 50% of our ultimate capacity, so there is still a good amount of room to grow. If you know someone that might benefit from our services, please let them know about us.

Looking Ahead

Before looking ahead to 2024, let’s revisit how we concluded last year’s annual review:

While 2022 marked the abrupt end to an era characterized by steady inflation, low interest rates, and debt-fuelled speculative investments, we remain optimistic about 2023 and the years beyond. While the global economy may continue to slow and various regions could fall into recession over the coming months, much of the potential bad news now seems to be priced into capital market valuations. If inflation continues to normalize, central banks should stop raising interest rates – or even contemplate rate cuts – and good economic news could once again become more plentiful.

In hindsight, these comments proved to be fairly accurate: inflation continued to normalize, central banks stopped raising interest rates, and by year end investors generally became more optimistic about the future.

As we move into 2024, a key question is how quickly inflation returns to target (i.e. 2%) and how this impacts central bank interest rate policy. Investors currently predict rate cuts to start in the first half of the year, which could be overly optimistic should the economy continue to perform above expectations and if inflation remains high as a result. There will also be a Presidential election in the United States in November, the outcome of which could have far-reaching implications for the world and capital markets.

There are many risks and opportunities on the horizon, but trying to predict future outcomes is impossible. Instead, we remain confident that over the long term investors are best served by remaining fully invested in low-cost passively-managed portfolios that are suitable for their circumstances given their financial objectives and risk tolerance. That may seem like unsophisticated advice, but it is advice that has undeniably served many investors well.

We wish everyone a prosperous year ahead and we look forward to playing a part in your continued success.