As a portfolio manager, our mission is to help clients allocate their money to investment portfolios that provide efficient risk-adjusted returns over the long-term. To achieve this, we conduct an annual review of our portfolio construction process, consisting of four main steps:

- Creating long-term capital market assumptions for various asset classes.

- Developing model portfolios with varying asset allocations to cover a range of risk/return characteristics.

- Reviewing the universe of available investment products and determining which ones to approve for use in our model portfolios.

- Mapping approved investment products to model portfolios across various account types to minimize costs and taxes.

This article focuses on the first step of the portfolio construction process: our updated long-term capital market assumptions for 2023.

What are Long-Term Capital Market Assumptions?

You can think of long-term capital market assumptions as the building blocks of an investment portfolio. To begin, we identify a list of asset classes that we might want to include in client portfolios. Our current list of approved asset classes includes:

| Fixed Income | Equity (Stocks) | Alternatives |

|---|---|---|

| Canada – Cash | Canada | Gold |

| Canada – Short-term Bonds | United States | |

| Canada – Universe Bonds | International – Developed Markets | |

| United States – High Yield Bonds | International – Emerging Markets | |

| Global – Low Volatility |

This year we started including assumptions for U.S. High Yield Bonds for the first time. High yield bonds are debt securities that typically pay higher interest rates because they are issued by corporations that have lower credit ratings than investment-grade bonds. We’ll have more to say about this new asset class in the near future.

For each approved asset class, we come up with a set of assumptions (i.e. forward-looking projections) for:

- Expected return: the average annual percentage return we expect to generate over the long term (i.e. 10+ years).

- Expected risk: a measure of the expected year-to-year volatility of the expected return.

- Expected correlation: the degree to which the values of any two asset classes are expected to move up or down in relation to each other.

Developing long-term capital market assumptions is a complex task typically undertaken by large institutional investors with teams of experts that develop financial models aimed at predicting the future path of interest rates, inflation, employment, and economic growth. Some firms develop capital market assumptions for their own internal purposes, but many publish reports detailing their findings. Each year we survey the publicly-available long-term capital market assumptions from trusted sources and consolidate them into our own set of assumptions. In rare circumstances we apply professional judgement to the consolidated data and make adjustments where we believe it is warranted, but for the most part we just let the data speak for itself.

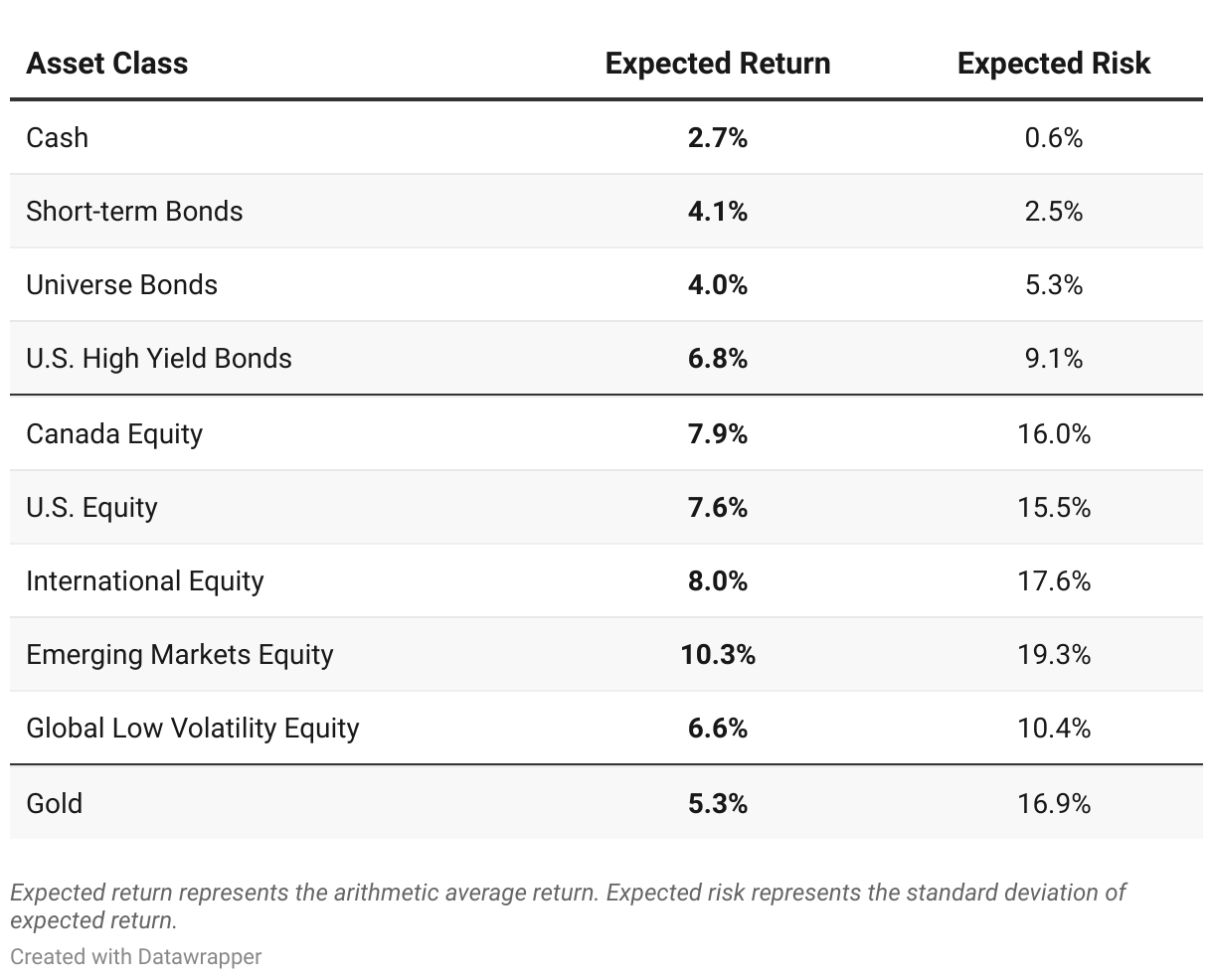

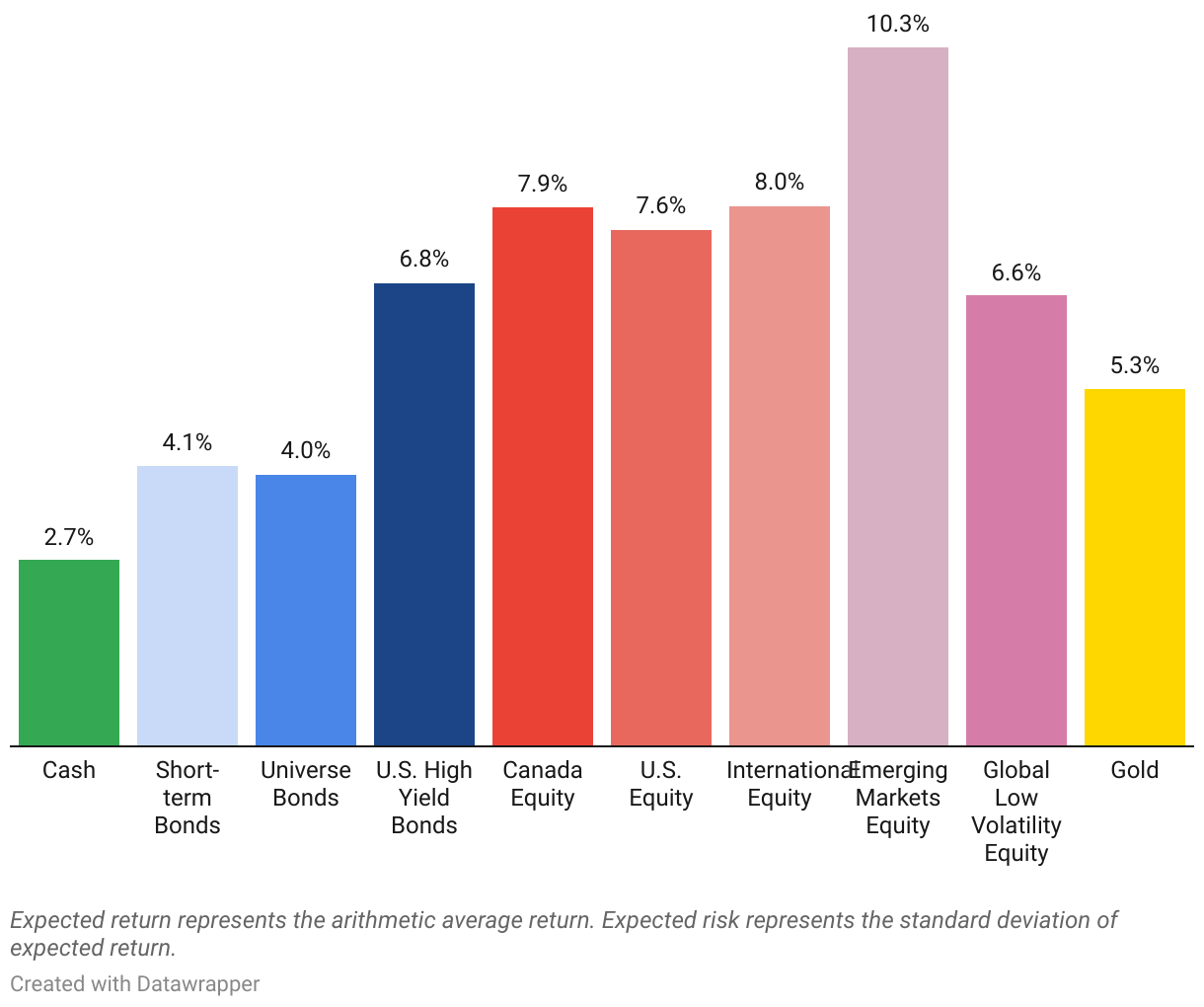

Our 2023 Long-Term Capital Market Assumptions

After completing the data collection process outlined above, we’ve updated our long-term capital market assumptions for 2023. While it is difficult to predict the future with a high degree of certainty, these assumptions represent our best guess of the returns (before fees or taxes) that a Canadian investor can reasonably expect to achieve on average when investing in various asset classes over the long term (i.e. 10+ years):

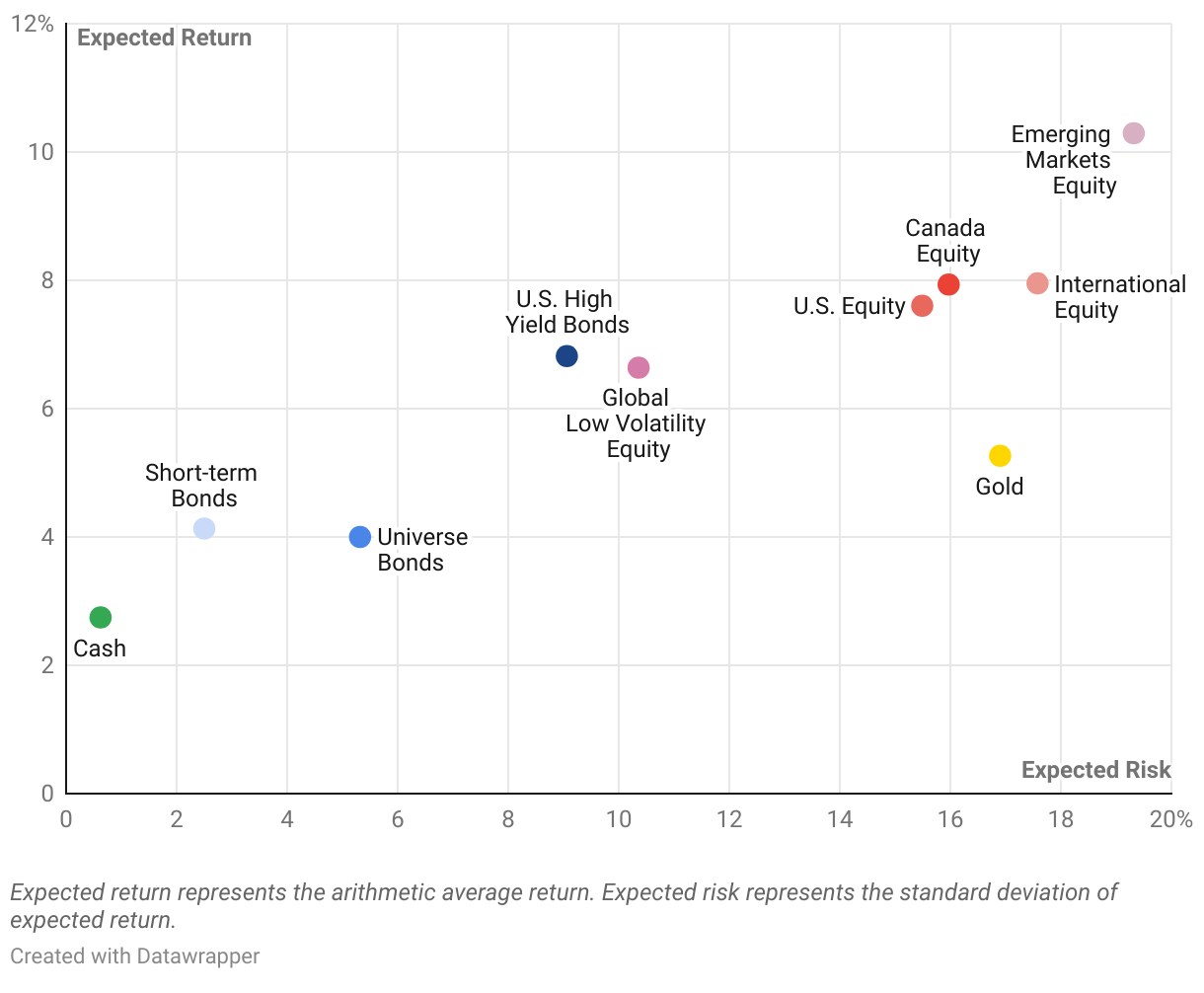

A useful way to visualize long-term capital market assumptions is to plot the intersection of expected return and expected risk for each asset class on a scatter chart. As demonstrated below, this highlights the clear relationship between return and risk – in order to earn a higher return, an investor generally needs to be willing to accept more risk:

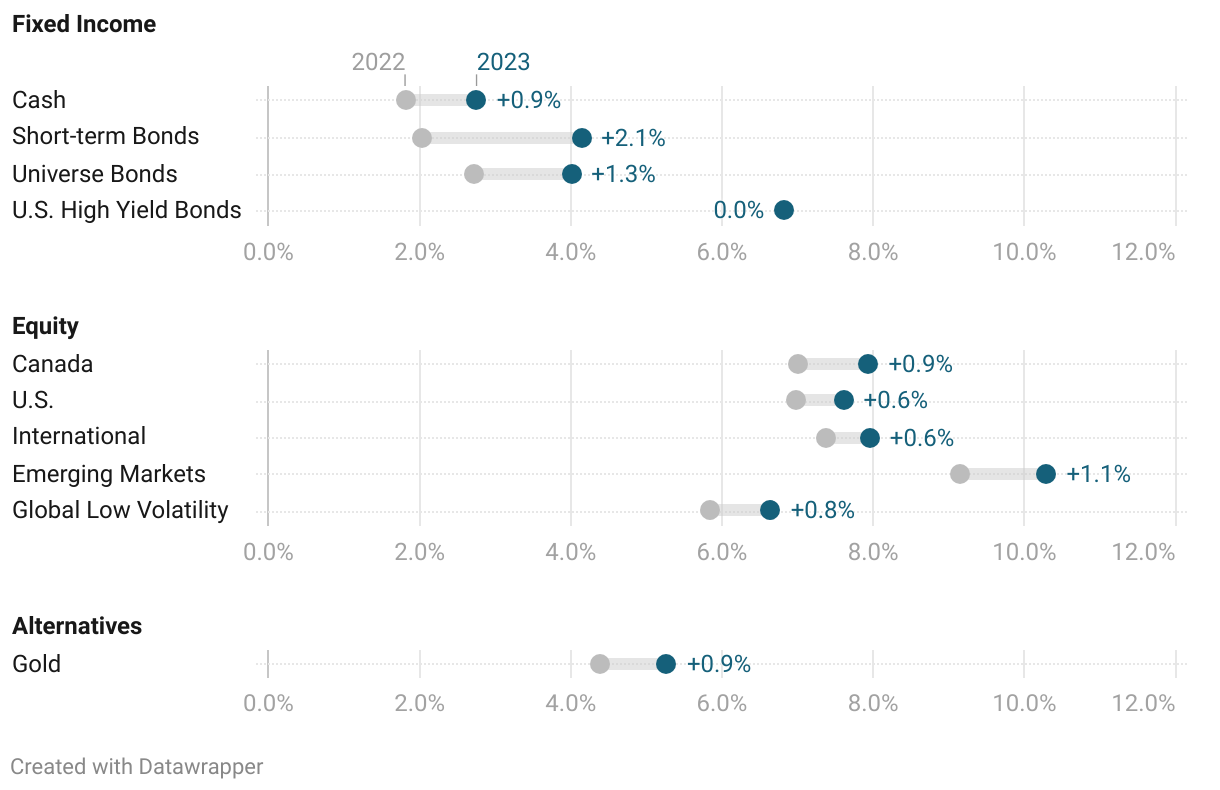

Changes to Expected Returns

As discussed more thoroughly in our article The Year in Review: 2022, capital markets performed poorly in 2022. While negative returns can be both painful and stressful in the moment, an often-overlooked side benefit is the improvement this makes to future return expectations. All else being equal, to the extent that fixed income and equity valuations decreased substantially last year, those asset class categories should be more attractive investments going forward.

The chart below compares the expected returns in our 2023 long-term capital market assumptions against the prior year, highlighting the changes for each asset class:

Higher Returns Expected for Fixed Income

Given the dramatic rise in interest rates since the start of 2022, it is not surprising to see further improvements to the long-term expected returns for fixed income asset classes this year. Compared to 2022, the expected return for Short-term Bonds has improved by an impressive 2.1% while the expected return for Universe Bonds has improved by 1.3%. These are encouraging developments for fixed income investors who had been grappling with record low yields in recent years and experienced negative returns in 2022. As this is the first year that we’ve included assumptions for U.S. High Yield Bonds, there is no prior-year comparison for that asset class.

Higher Returns Expected for Equity

The negative performance experienced across equity asset classes in 2022 reduced their valuation metrics, providing a more attractive starting point for forward-looking return projections in our 2023 long-term capital market assumptions. Expected returns have therefore increased for all equity asset classes this year, ranging from +0.6% to +1.1%.

Conclusion

Hopefully this article has provided insight into how we arrive at our long-term capital market assumptions and how these assumptions serve as the building blocks for our investment portfolios. With significant increases to long-term expected returns across all asset classes in 2023, the go-forward prospects for clients’ investment portfolios look bright, which should be some consolation for the poor investment performance experienced in 2022. If you have any questions or would like to discuss this topic in more detail, please contact your advisor.