As a portfolio manager, our mission is to help clients allocate their money to investment portfolios that provide efficient risk-adjusted returns over the long-term. To achieve this, we conduct an annual review of our portfolio construction process, consisting of four steps:

- Creating long-term capital market assumptions for various asset classes.

- Developing model portfolios with different allocations to these asset classes, covering a range of risk/return characteristics.

- Reviewing the universe of available investment products and determining which ones to approve for use.

- Mapping the approved investment products to our model portfolios across different account types to minimize costs and taxes.

This article focuses on the second step of the portfolio construction process and our updated model portfolios for 2023.

What is a Model Portfolio?

Before discussing our model portfolios in more detail, let’s first define what we mean when we use the term model portfolio. A model portfolio is a set of asset class allocations (or weightings) used to guide the investment of a client’s money at a high level, before any security-specific implementation decisions are made. Since the allocations are assigned at the broad asset class level, model portfolios are theoretical and it is not possible to invest in them directly. However, model portfolios are useful because they allow us to assess risk/return characteristics and construct portfolios using a limited number of inputs rather than having to consider the full universe of available investment products, which number in the thousands.

New for 2023: U.S. High Yield Bonds

We included United States High Yield Bonds in this year’s long-term capital market assumptions and approved the asset class for inclusion in our model portfolios. High yield bonds are debt securities that typically pay higher interest rates because they are issued by corporations that have lower credit ratings than investment-grade bonds. The addition of U.S. High Yield Bonds was compelling for several reasons:

Favourable Return/Risk Characteristics

From a return/risk perspective, high yield bonds are positioned between investment-grade bonds and equities, offering higher expected returns than the existing fixed income asset classes in our model portfolios while simultaneously offering lower expected risk than the equity asset classes in our model portfolios. U.S. High Yield Bonds therefore provide a useful middle ground when constructing portfolios.Enhanced Risk-Adjusted Portfolio Returns

Historically, there has been low correlation between U.S. High Yield Bonds and the fixed income asset classes previously approved for use in our model portfolios (i.e. Cash, Canada Short-term Bonds, and Canada Universe Bonds). Assuming the relationship holds, adding U.S. High Yield Bonds should enhance overall portfolio returns with only a moderate increase to overall portfolio risk, resulting in higher risk-adjusted returns over the long-term.Increased Diversification

Prior to this year’s review, the fixed income allocation of our model portfolios was limited to Canadian bond issuers. This is reasonable for government bonds given the high correlation between Canadian interest rates – the main driver of government bond performance – and interest rates in other developed countries. For example, holding either Canadian government bonds or currency-hedged U.S. treasuries should both provide relatively similar returns over time.However, the performance of corporate bonds is affected not only by interest rates but also by default risk – the possibility that a bond issuer fails to make interest or principal payments on time. From this perspective, limiting the fixed income allocation of our model portfolios to Canadian issuers is suboptimal and shifting a portion of the allocation to U.S. High Yield Bonds increases diversification with exposure to hundreds of additional bond issuers.

Suitability and Costs

There are a multitude of asset classes to choose from when constructing an investment portfolio but we limit the list of approved asset classes for our model portfolios to a relatively small number – currently ten – to ensure that costs are kept reasonable and undue complexity is avoided. Before approving a new asset class, it must be evaluated against our suitability criteria using such factors as market size, availability of long-term return/risk/correlation data, trading costs/market liquidity, product fees, and price transparency. The U.S. high yield bond market is well-established and there are investment products (i.e. exchange-traded funds) tied to the asset class that meet our suitability and cost criteria.

Portfolio Optimization

Using our approved asset classes as building blocks and assuming the allocation for each asset class can range from 0% to 100% (in 1% increments), there are more than 1 trillion possible model portfolios. It wouldn’t be practical to manually evaluate the risk and return characteristics for each of these possibilities, but thankfully technology can assist us.

We input our long-term capital market assumptions and a set of minimum diversification constraints into portfolio optimization software. The software analyzes all possibilities using the modern portfolio theory framework to eliminate inefficient model portfolios – a portfolio is considered inefficient if any substitute portfolios exist that 1) provide a higher return for the same level of risk, or 2) provide the same return with a lower level of risk. When the optimization process has completed, the software outputs what is know as an efficient frontier: the set of model portfolios expected to provide the highest return at each possible level of risk.

We select a subset of the portfolios along the efficient frontier as our model portfolios, which are then used during investment suitability assessments with our clients, allowing us to provide a broad, but manageable, range of risk/return investment options.

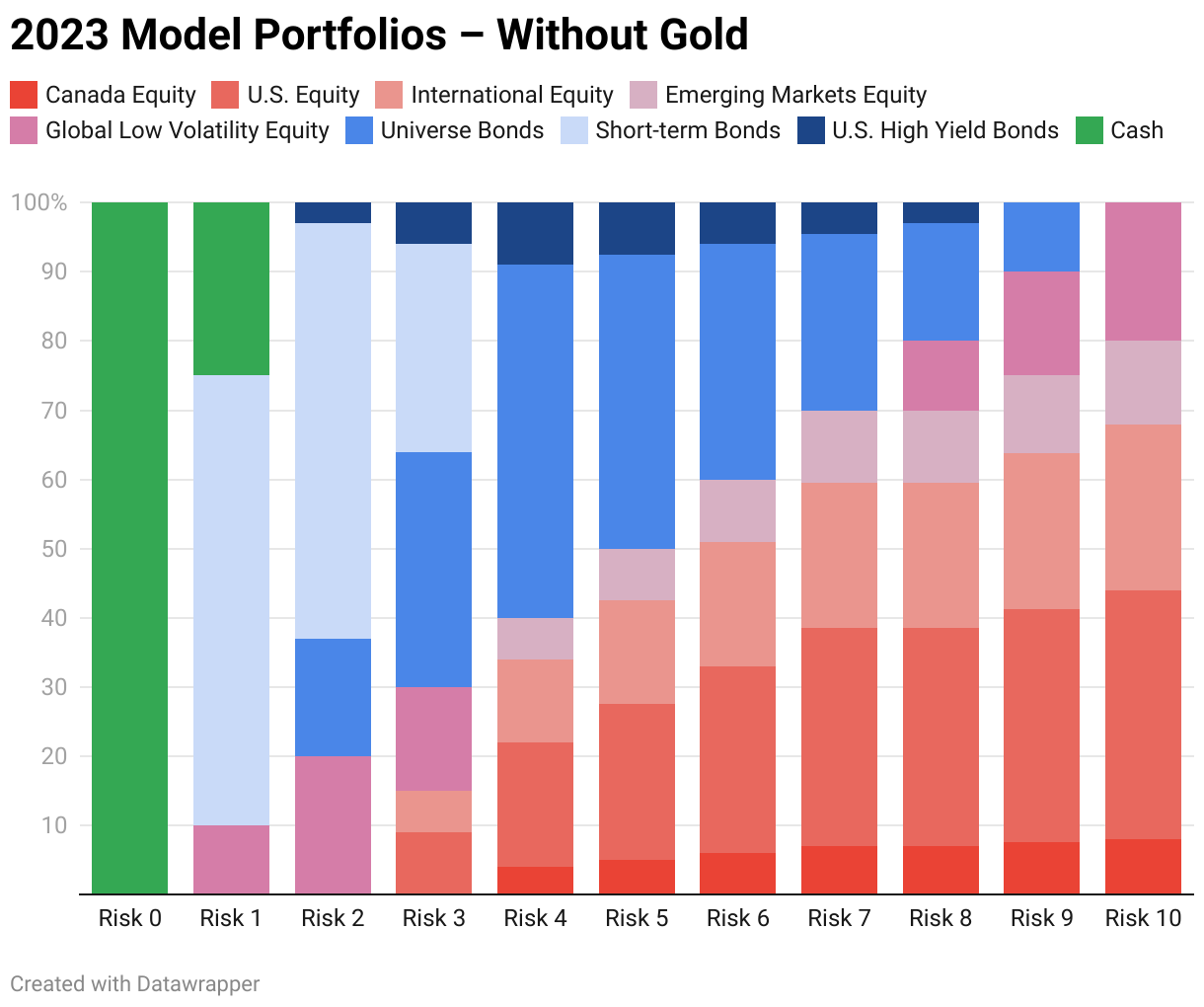

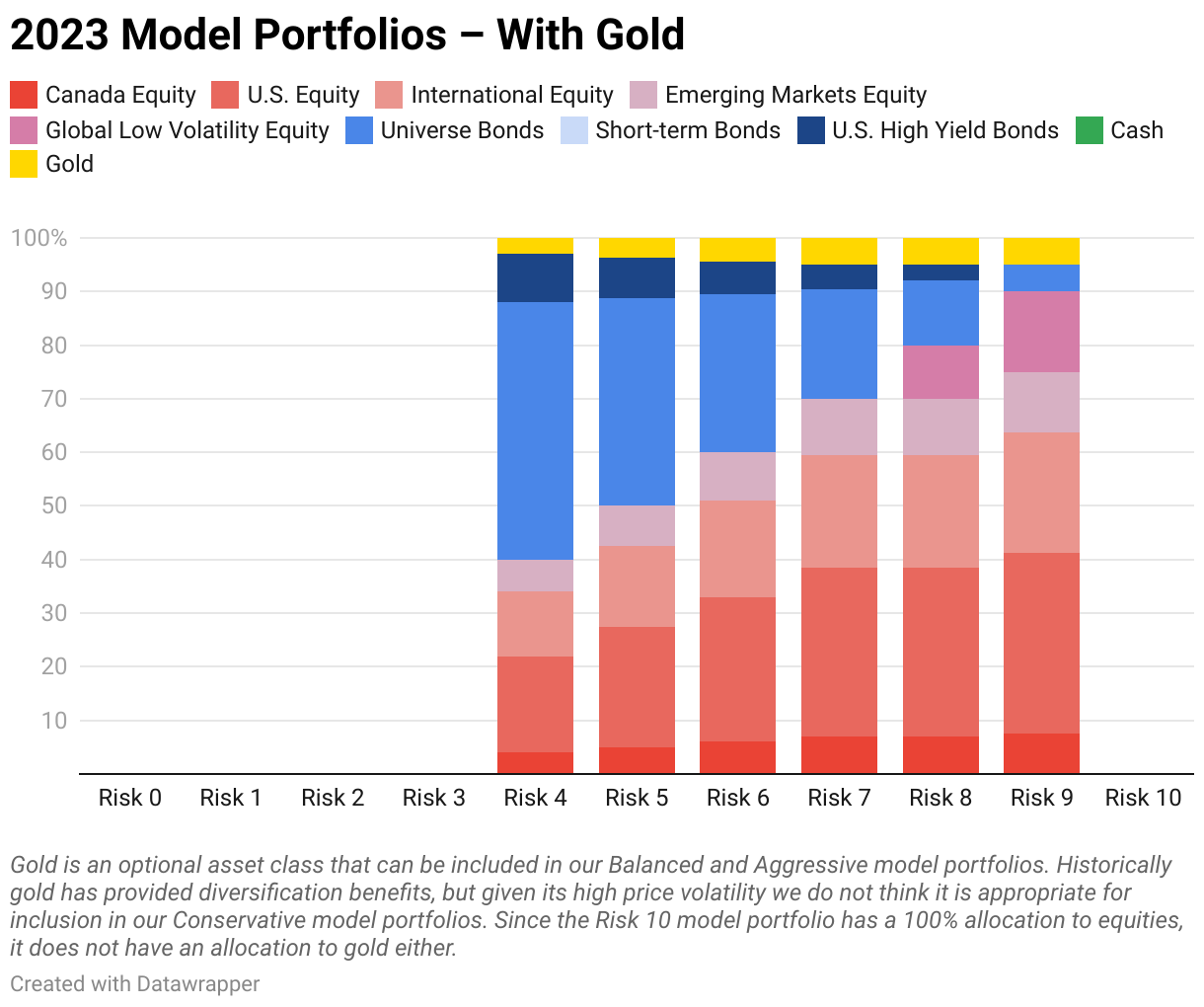

Our 2023 Model Portfolios

After completing the portfolio optimization process outlined above, we’ve updated our model portfolios for 2023, split into two groups: those with an allocation to gold and those without. While it is not possible to predict the future with certainty, these model portfolios represent our best guess of the asset allocations that a Canadian investor can expect to provide the highest returns for given levels of risk over the long-term:

Changes to Model Portfolio Allocations

The changes outlined in our 2023 long-term capital market assumptions and the introduction of U.S. High Yield Bonds as a new approved asset class have resulted in revisions to the majority of our model portfolios this year:

Risk Level 1

Shifted 25% from Short-Term Bonds to Cash.Risk Level 2

Shifted 18% from Universe Bonds to Short-Term Bonds (+15%) and U.S. High Yield Bonds (+3%).Risk Level 3

Shifted 5% from Global Low Volatility Equity to U.S. Equity (+4%) and International Equity (+1%). Shifted 21% from Universe Bonds to Short-Term Bonds (+15%) and U.S. High Yield Bonds (+6%).Risk Levels 4-8

Shifted varying allocations from Universe Bonds to U.S. High Yield Bonds, calculated as 15% of each model portfolio’s non-equity (i.e. fixed income + gold) asset allocation.

Client portfolios will be transitioned to align with our new model portfolios in the near future. Your advisor will be in contact with you to provide additional details.

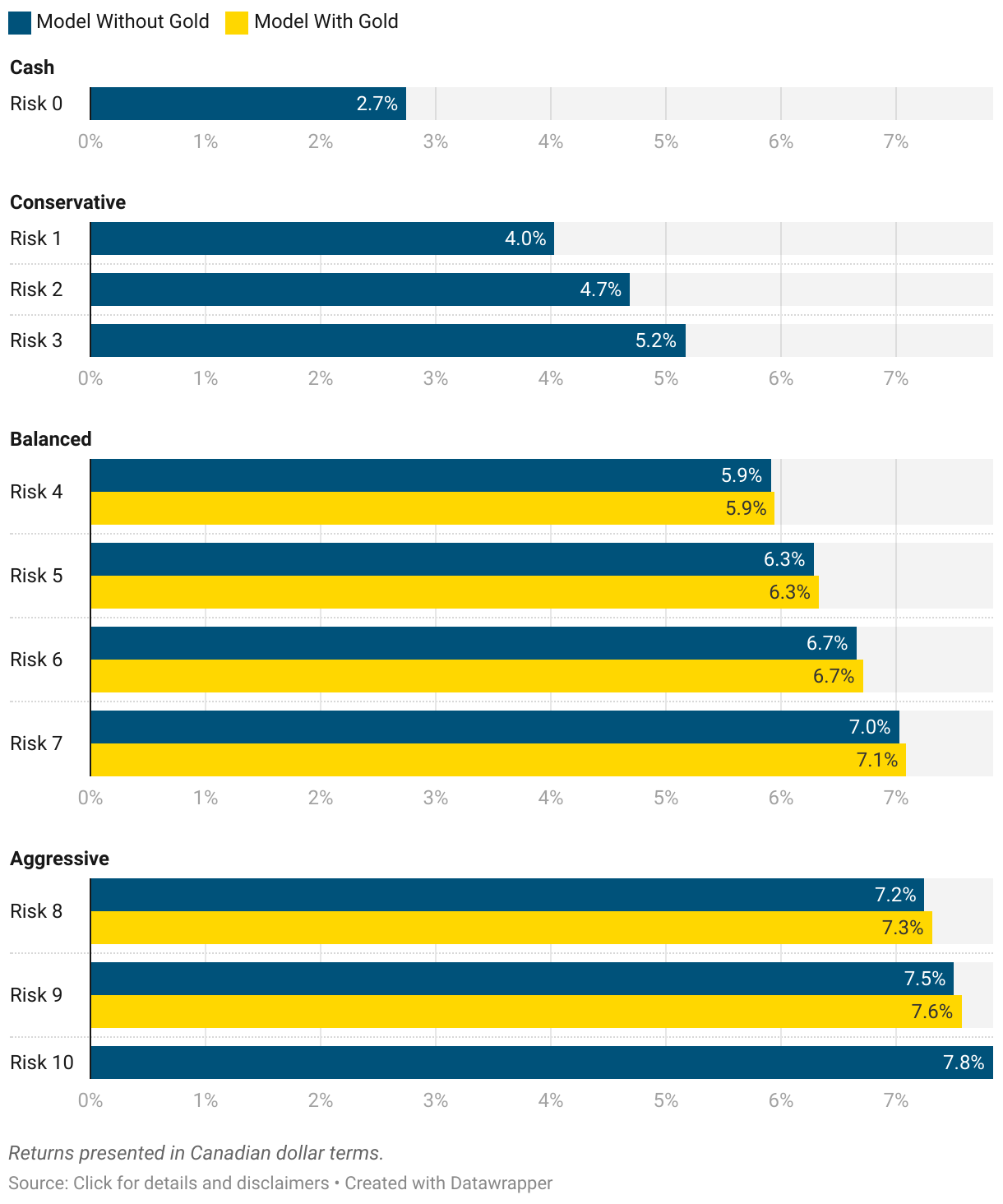

Model Portfolio Return Assumptions

By combining the model portfolio asset allocations outlined above with our 2023 long-term capital market assumptions we can calculate the weighted-average expected return for each of our 2023 model portfolios. While it is not possible to predict the future with certainty, these assumptions represent our best guess of the returns (before fees or taxes) that a Canadian investor can expect to achieve over the long-term by investing in a portfolio of securities with an asset allocation similar to that of each model portfolio:

Our model portfolio return assumptions play a key role in financial planning. Once we have completed an investment suitability assessment and allocated model portfolios to a client’s investment accounts, we update the assumptions in their financial plan to reflect the expected return of their actual investments. Working with a portfolio manager that provides both financial planning and investment management ensures consistency between the two elements.

Our goal in writing this article was to provide insight into what a model portfolio is, how we analyze the many combinations of possible asset class allocations that make up a model portfolio, and how we filter down the many possibilities into a manageable set of model portfolios that cover a range of risk and return characteristics. If you have any questions or would like to discuss these topics in more detail, please contact your advisor.