If you opened a newspaper, turned on the radio, watched TV, or browsed the web this week you probably noticed a few headlines like these:

“Coronavirus Drives Down Stocks for 6th Day, Nearing a Correction”

“Stocks Slide Toward a Correction as Virus Fears Show No Sign of Easing”

“BREAKING: Dow plunges as many as 960 points”

“TSX drops over 2% as coronavirus fear grips stocks, oil”

“What the Street is saying as markets continue to tumble”

Constant exposure to these worrying headlines inevitably raises questions about your own investments and whether you should be doing anything to react. If governments around the globe are taking precautions to protect their citizens from a potential pandemic, shouldn’t we be taking actions to protect our investment portfolios as well?

Here are three ways of answering that question:

In a word: No.

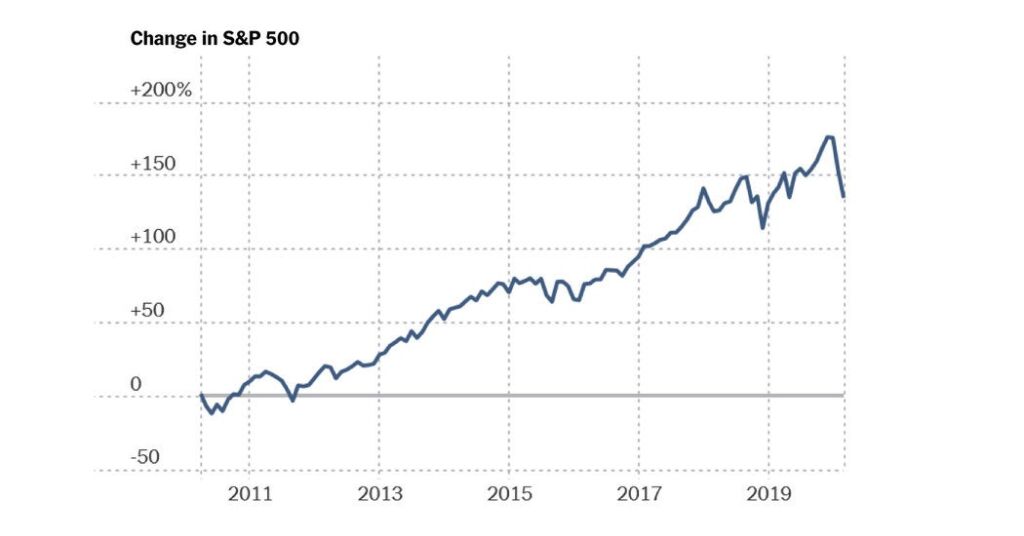

In a sentence: Market timing – especially when driven by emotion – increases trading costs, potentially increases taxes, and often leads to buying high and selling low, the exact opposite of the outcome you’re trying to achieve.

In a thousand words:

Now that we’ve all taken a deep breath, let’s talk about what you can focus on instead of the sensational news headlines:

Have an appropriate asset allocation

As this week’s events highlight, when the stock market corrects it tends to do so without any warning, leaving investors with little time to react. It is therefore important to have an appropriate asset allocation (the mix of stocks, bonds, cash, and other asset classes in your portfolio) in place before anything bad happens. As part of our process, we work with our clients to determine an appropriate asset allocation based on their risk tolerance (their psychological willingness to take risk), their risk capacity (their ability to withstand any negative outcomes), and their required risk (the risk needed to achieve a desired investment return).

Reduce investment fees

While we can’t control the day-to-day fluctuations of the stock market, there are other things we can control, like investment fees. The typical mutual fund in Canada charges fees of about 2% per year. Investment products called segregated funds offered by insurance companies charge fees closer to 3% or more per year. On the other hand, many exchange-traded funds (ETFs) are now available with fees of about 0.2% per year and working with an investment manager that invests in ETFs on your behalf will typically cost another 0.5% to 1% per year. Following this latter approach and reducing your investment fees by 1% to 2% each year can have a dramatic positive impact on your wealth over time.

Have a financial plan

Investing without a financial plan is like starting a road trip without a map. Your financial plan provides an outline for how much you’ll need to save, what asset classes you should invest in, how much insurance you might need, how taxes will affect your wealth, and answers any “what-if” questions you might have about your financial future. When the stock market corrects, the results can be viewed through the lens of your financial plan, allowing you to focus on the long-term impact rather than focusing on sensational short-term headlines.