As a discretionary portfolio management firm, we strive to deliver strong long-term investment returns while carefully managing risk. To achieve this goal, we regularly review and update our investment portfolios through a four-step process:

- Establishing assumptions: defining long-term capital market assumptions for our approved asset classes.

- Developing model portfolios: blending approved asset classes in various weightings to offer a range of risk/return profiles.

- Selecting products: evaluating investment products to determine which ones to include in client accounts.

- Mapping for efficiency: mapping approved investment products to model portfolios across different account types to maximize tax efficiency and minimize costs.

This article focuses on the second step: reviewing and updating our model portfolios for 2026.

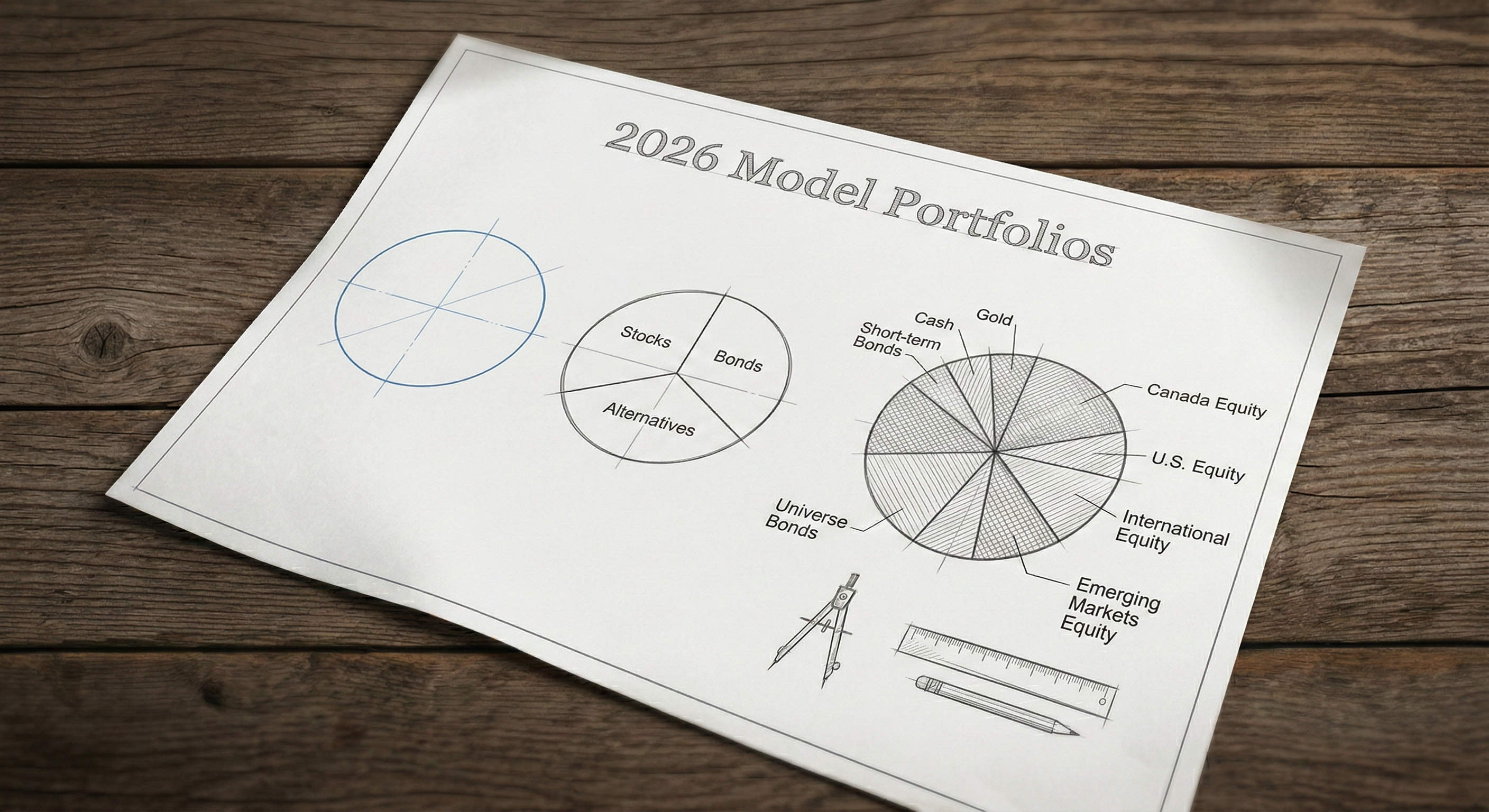

What is a Model Portfolio?

Before diving into the details, let’s define the term model portfolio. In short, it is a high-level blueprint of asset class allocations (or weightings) used to guide how we invest a client’s money.

Because allocations are assigned at the broad asset class level (e.g. “Canadian Equities” or “Short-Term Bonds”), model portfolios are theoretical – you cannot invest in them directly without eventually buying specific securities or funds. However, model portfolios are incredibly useful. They allow us to assess risk and return characteristics using a manageable set of broad inputs rather than sorting through thousands of individual investment products right from the start.

Optimization

If we use our ten approved asset classes as building blocks and allow the weight of each to range anywhere from 0% to 100% (in 1% increments), the number of possible model portfolios is nearly endless. Because it isn’t practical to manually evaluate the risk and return characteristics for so many possibilities, we use technology to streamline the task.

We feed our long-term capital market assumptions and a set of minimum diversification constraints into portfolio optimization software. Using mean-variance analysis, the software analyzes all possible asset combinations to eliminate “inefficient” portfolios. (A portfolio is considered inefficient if another option provides a higher return for the same amount of risk, or the same return for less risk). When the optimization is complete, the software produces an efficient frontier representing the set of portfolios expected to provide the highest return for a given level of risk.

We select a subset of portfolios along (or very close to) the efficient frontier to serve as our model portfolios, allowing us to offer a diverse range of investment options built on a repeatable, evidence-based process.

2026 Model Portfolios

After completing the optimization process, we’ve updated our model portfolios for 2026. To accommodate different investor preferences, we have split them into two distinct groups: models with an allocation to gold, and those without. While it is impossible to predict future market movements with absolute certainty, these model portfolios represent our baseline expectations for the asset allocations that will provide Canadian investors with attractive, long-term returns for chosen levels of risk:

Changes to Model Portfolio Allocations

Despite significant updates to our 2026 long-term capital market assumptions, we did not make any adjustments to our model portfolio asset allocations this year. The current allocations continue to offer expected return and risk characteristics that lie close to the newly forecasted efficient frontier, meaning no changes are warranted.

Model Portfolio Return Assumptions

By applying our 2026 long-term capital market assumptions to these asset allocations, we can project an expected return for each model portfolio. While no one can predict the future with absolute certainty, the figures below represent our baseline expectations for the average annual returns (before fees or taxes) that Canadian investors can expect to achieve over the long term (10+ years) when investing in similar portfolios:

Changes to Model Portfolio Expected Returns

As discussed in our recent article, The Year in Review: 2025, capital markets just delivered a third consecutive year of impressive gains. However, a byproduct of such sustained, above-trend performance is a lowering of future return expectations. This dynamic is reflected in our latest assumptions, with expected returns declining by approximately 1% across most model portfolios. The charts below compare the expected returns for our 2026 model portfolios against the previous assumptions and highlight the impact for each model portfolio:

Conclusion

As we’ve outlined, model portfolios are the blueprint we use to filter endless investment possibilities into a manageable, risk-adjusted lineup for our clients. While our 2026 update reflects a broad reduction of approximately 1% in expected returns across most of these models, it is important to remember that this is the natural byproduct of three consecutive years of impressive market gains. Despite the tempered expectations, the go-forward prospects for our portfolios remain solid.

Ultimately, these return assumptions play a vital role in your financial planning. After assessing your investment suitability and assigning the right model portfolio to each of your accounts, we update your financial plan to reflect the associated expected returns. Working with a firm that provides both financial planning and investment management ensures consistency between your goals and your portfolio.

If you have any questions about these 2026 updates please contact your advisor.